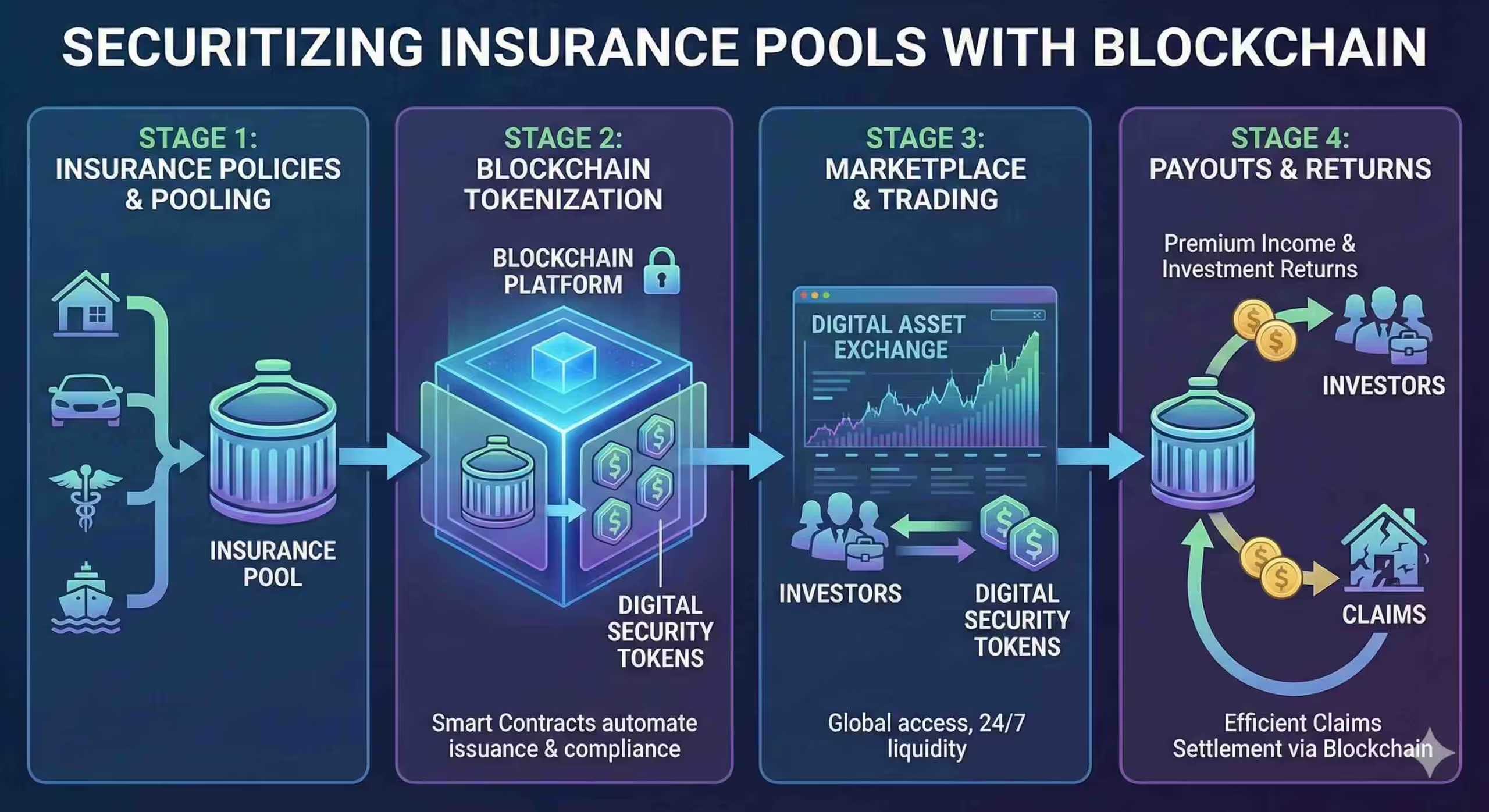

Blockchain technology offers transformative potential for the insurance industry by enabling the securitization of Insurance pools, which consist of premiums collected from policyholders, that can be bundled and securitized into tradeable financial assets on blockchain platforms. This process is similar to how mortgages or loans are bundled into securities in traditional finance. Insurers convert portions of their risk exposure into securities, known as InsuranceLinked Securities (ILS), which can then be sold to investors.

Table of Contents

Bundling and Tokenizing Insurance Pools:

For example, XYZ Insurance collects premiums from policyholders, creating a substantial insurance pool. Traditionally, this pool would be held in reserve to cover potential claims. However, with blockchain technology, XYZ Insurance can tokenize these insurance pools into tradable financial assets called Insurance-Linked Securities (ILS).

Creating Insurance-Linked Securities (ILS):

XYZ Insurance uses blockchain to create digital tokens representing portions of its insurance pool. Each token represents a share of the risk associated with the pool. For instance, if XYZ Insurance has a $100 million insurance pool, it can tokenize this into 10 million tokens valued at $10 each.

Trading on Secondary Markets:

These tokens are then listed on blockchain-based trading platforms, where investors such as pension funds or hedge funds can buy and sell them. Investors are attracted by the potential for high returns, which come from receiving premiums or interest payments from the insurance pool. This trading provides immediate liquidity to XYZ Insurance.

Capital Efficiency:

By selling these tokens, XYZ Insurance offloads part of its risk to the capital markets. Hence, tokenization frees up capital for the insurance company that would otherwise be tied up as reserves in the balance sheet. For example, if XYZ Insurance sells 50% of its tokens, it effectively releases $50 million in capital.

Expanding Coverage:

With the freed-up capital, XYZ Insurance can now expand its coverage, underwrite more policies, or invest in new areas. This increased efficiency helps improve overall operational capacity and financial stability.

The Mechanics of Blockchain Insurance Securitization

| Step Name | Description of Action | Role of Blockchain & Smart Contracts |

| Risk Pooling & Aggregation | An insurer or reinsurer bundles a specific set of policies (e.g., 1,000 Florida home insurance policies) into a “pool” to transfer the risk. | Immutable Record: The details of every policy in the pool are hashed and recorded on-chain for transparency and auditability. |

| SPV Creation (Smart Contract) | A Special Purpose Vehicle (SPV) is created to hold these risks separate from the insurer’s balance sheet. | Digital SPV: Instead of expensive legal entities, a Smart Contract acts as the automated custodian, defining the rules of the pool. |

| Tokenization | The value of the insurance pool is divided into digital tokens. These are security tokens representing a share of the risk and potential reward. | Token Minting: The protocol mints ERC-20 (or similar) security tokens. These can be fractionalized, allowing smaller investors to participate. |

| Capital Raising (STO) | Investors purchase these tokens using cryptocurrency or stablecoins. The capital raised is held as collateral to pay potential claims. | Instant Settlement: Investors receive tokens immediately upon payment. No T+2 day wait times; the ledger updates instantly. |

| Premium Flow & Yield | Policyholders pay premiums. These funds are passed to the SPV to pay interest (yield) to the token holders/investors. | Automated Dividends: Smart contracts automatically distribute the premium income to token holders’ wallets in real-time or at set intervals. |

| The Trigger Event (Oracle) | A specific event occurs (e.g., a hurricane hits). The system must decide if a payout is due. | Oracles: Trusted data feeds (e.g., Chainlink) connect real-world data (wind speed, flood levels) to the blockchain to trigger the contract automatically. |

| Execution & Settlement | Scenario A (No Disaster): The contract matures, and investors get their principal back + interest. Scenario B (Disaster): Collateral is used to pay the insurer’s claims. | Trustless Execution: The code executes the payout immediately based on the Oracle data. No human intervention or claims adjusting delays are required. |

Presently, insurance penetration remains low, at 4.2% of GDP in 2022. Using blockchain securitization can help insurers manage large-scale risks more efficiently while improving solvency ratios.